For UK and European startup entrepreneurs venturing into American markets, understanding how U.S. venture capital firms operate isn’t just helpful—it’s essential for success. This guide breaks down the economic machinery driving U.S. venture capital decisions and outlines how European startups can position themselves effectively in this competitive landscape.

Why American Capital Matters for European Innovation

The numbers speak for themselves. U.S. VCs deployed over $140 billion in 2024—more than double Europe’s $60 billion. But this isn’t just about bigger checks. American capital brings networks that can transform European startups into global contenders.

U.S. VCs operate with different incentives and expectations than their European counterparts. Their economic model creates distinct pressures and priorities that shape how they evaluate businesses, and understanding these dynamics gives European founders a critical edge when pitching.

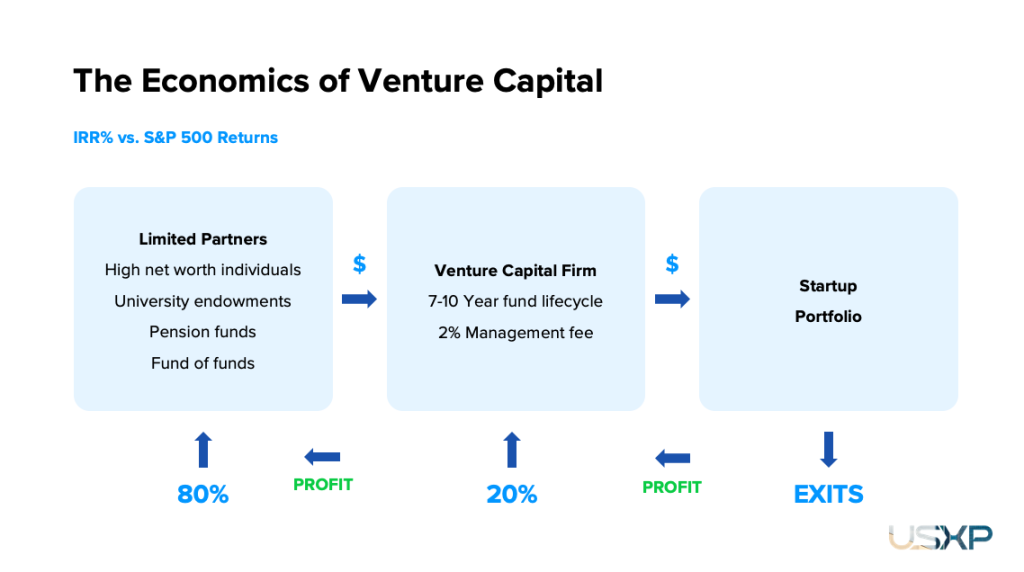

Limited Partners: Who Funds U.S. VC Firms?

Limited Partners (LPs) are the entities who provide the capital that VC firms invest in startups. The money flowing through American VC firms comes primarily from four sources:

- High net worth individuals: Silicon Valley and New York wealth with deep experience in technology investment

- University endowments: Institutions like Harvard and Stanford with decades of venture investing history

- Pension funds: Major systems like CalPERS that allocate significant capital to alternative investments

- Funds of funds: Investment vehicles that spread risk across multiple VC portfolios

This LP structure differs significantly from Europe, where government funds and corporate investors play a more prominent role. This shapes expectations in meaningful ways. American VCs answer to LPs who demand “unicorn” outcomes and have less patience for the steady, moderate-growth businesses that might find backing in London or Berlin.

The 7-10 Year Clock: Fund Lifecycles and Your Timeline

U.S. venture capital operates on a strict timeline—funds typically deploy capital into startups for 3-5 years, then spend the remaining years managing investments toward exits. This puts tremendous pressure on VCs to identify winners quickly.

For European startups, this creates both opportunity and challenge. American VCs can accelerate entry into U.S. markets through their networks, but they’ll expect rapid scaling in return. Many European founders are caught off guard by the pace American investors expect; preparing to demonstrate significant milestones within their timeframe is critical. If a startup isn’t showing significant traction within a few years, they may shift their focus to other portfolio companies. To keep their support, you’ll need to demonstrate consistent growth and a clear path to a U.S.-style exit.

Following the Money: The 2 & 20 Model

The economics of U.S. venture capital revolve around a simple but powerful model:

- 2% management fee: Annual operating expenses pulled from committed capital

- 20% carried interest: The VC’s share of profits after returning initial capital

This structure is similar to what exists in Europe, but the implications run deeper in the U.S. market. A typical $500 million American fund generates $10 million annually in management fees—supporting expensive Silicon Valley offices and specialized staff.

The “carry” is where fortunes are made. This 20% profit share creates powerful incentives to pursue outsized returns rather than modest successes. Many European founders initially pitch “reasonable” growth trajectories that would satisfy European investors but fail to excite American VCs hunting for the next Uber or Airbnb.

The Power of Carried Interest

Carried interest aligns VC interests with potential for explosive growth. Since VCs only collect their 20% after returning capital to LPs (often with an 8% minimum return hurdle), they’re focused exclusively on companies that can deliver substantial multiples.

This explains why U.S. VCs might pass on profitable European businesses with “mere” 2-3x return potential. American VCs aren’t being unreasonable when they push for aggressive growth—they’re responding to their economic incentives.

The S&P 500 Benchmark Challenge

American VC funds face a demanding benchmark: the S&P 500 Index. With historical returns of 7-10% annually, this high-performing index sets a baseline that venture capital must significantly exceed to justify its risk profile.

Successful U.S. VC funds target IRRs of 20-30% or higher. However—and this surprises many European founders—only about 25-30% of American VC funds consistently outperform the S&P 500 after fees. The vast majority either match or underperform the broader market.

This creates relentless pressure for VCs to identify truly exceptional opportunities. When pitching to American investors, European startups aren’t just competing against other startups; they’re competing against the S&P 500 itself. Growth stories need to convince VCs that they represent the kind of outlier investment that can help them beat this challenging benchmark.

Winning American Investment: Essential Checklist for European Founders

For European startups seeking U.S. venture capital, thorough preparation across these key areas dramatically improves fundraising outcomes:

- Understanding US VC Expectations & Market Norms: Recognize that American VCs operate under different pressures than European counterparts. They need to outperform the S&P 500 and deliver returns that justify their fee structure, creating a higher bar for investment. Successful European founders study how leading U.S. startups position themselves and adapt their approach accordingly.

- US-Focused Pitch Deck & Market Sizing: Develop presentation materials that specifically address the American market opportunity. This means conducting detailed U.S. market analysis, sizing the opportunity in billions rather than millions, and demonstrating deep understanding of the competitive landscape. American VCs expect market sizing that supports potential billion-dollar outcomes.

- Consolidated Pro Forma Financial Model: Create comprehensive financial projections that reflect U.S. market realities—including higher customer acquisition costs, more aggressive hiring plans, and faster scaling timelines. American VCs typically expect to see projections showing the path to $100M+ ARR, with clear unit economics and capital efficiency metrics.

- Data Room Based on US-Style Due Diligence Request List: Prepare documentation that meets American investor expectations for thoroughness and transparency. This includes U.S.-style capitalization tables, customer contracts, employment agreements, and IP documentation. European founders often underestimate the level of detail and formality required in U.S. due diligence processes.

- US GTM Playbook and Year 1 Operating Model: Develop a detailed, executable plan for entering and scaling in the American market. This should include specific customer acquisition strategies, pricing models adapted for U.S. customers, channel partnerships, and hiring plans for U.S.-based team members. VCs want to see concrete operational plans, not just high-level strategy.

- US Investor Outreach and Warm Introductions: Map the American VC landscape to identify firms with relevant sector expertise and international portfolio experience. Securing warm introductions through mutual connections dramatically increases response rates. Cold outreach typically yields poor results in the relationship-driven U.S. venture community.

- US-Style Term Sheet Negotiations: Familiarize yourself with standard American term sheet provisions, which often differ from European norms. This includes liquidation preferences, anti-dilution protections, board composition, and founder vesting schedules. Being prepared for these discussions signals professionalism and helps avoid misunderstandings that can derail fundraising.

European founders who master these seven essentials transform from interesting foreign startups to compelling global opportunities worthy of American investment. Each element directly addresses the economic pressures U.S. VCs face from their limited partners and fund structures.

Bridging Two Worlds

European founders who understand American VC economics dramatically improve their fundraising outcomes. The U.S. venture ecosystem operates with different parameters than Europe’s—not better or worse, just different.

The American VC model creates unique pressures: funds need massive wins to justify their structure and beat the S&P 500. By aligning pitches with these realities, European startups transform from interesting regional players to compelling global opportunities deserving of American capital.

The startups that succeed in raising U.S. venture funding aren’t necessarily the most innovative or even the most profitable—they’re the ones that best understand and address the economic incentives driving American VC decisions. Mastering this perspective unlocks the capital and connections that can catapult European startups onto the global stage.

If you’re a Founder planning on raising your next round of VC in the US and have questions, please feel free to contact us today.