This is a guest blog post by Michael Holland with Blick Rothenberg.

Funding working capital of US Subsidiaries.

When UK businesses establish a new US subsidiary, one common practice is to provide loans from the parent company to the subsidiary. While this is straightforward in the UK, it becomes more complex in the US due to the Internal Revenue Service (IRS) regulations.

In the US, the IRS scrutinizes these loans to determine whether they should be classified as debt or equity. This classification has significant tax implications. If the IRS deems the loan to be equity, the interest payments made by the subsidiary to the parent company are not deductible, which can increase the subsidiary’s taxable income.

The IRS uses several key criteria to determine whether a relationship is debt or equity under Section 385:

- Unconditional Promise to Pay: The loan must include a clear, unconditional promise to repay a sum certain on demand or at a fixed maturity date.

- Creditor’s Rights: The lender must have the rights of a creditor to enforce the payment of principal and interest.

- Reasonable Expectation of Repayment: There must be a reasonable expectation that the subsidiary can and will repay the loan based on its financial position at the time of issuance.

- Actions Evidencing a Debtor-Creditor Relationship: The behavior of both parties should reflect a typical debtor-creditor relationship, such as timely payments and enforcement of default provisions.

Understanding these criteria and ensuring that loans are structured to meet them can help UK businesses avoid the reclassification of debt as equity by the IRS, thereby maintaining the tax benefits of interest deductions.

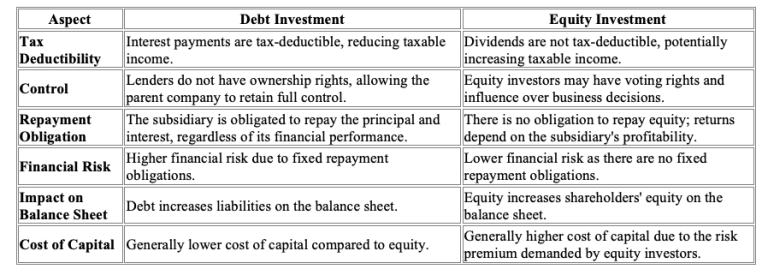

Pros and Cons of Debt vs. Equity Investment

To further clarify the implications, here is a comparison of the pros and cons of debt versus equity investment:

Consequences of Debt Being Deemed Equity

If the IRS reclassifies a loan as equity, the consequences can be significant:

- Loss of Interest Deduction: The subsidiary loses the ability to deduct interest payments, leading to higher taxable income and increased tax liability.

- Recharacterization of Payments: Payments that were intended as interest may be recharacterized as dividends, which are not tax-deductible and may be subject to withholding tax.

- Impact on Financial Statements: The reclassification can affect the subsidiary’s financial statements, altering the debt-to-equity ratio and potentially impacting creditworthiness and borrowing capacity.

Conclusion

Navigating the complexities of US tax regulations is crucial for UK businesses with US subsidiaries. By understanding the IRS criteria for classifying debt and equity and structuring loans accordingly, businesses can maintain the tax benefits of interest deductions and avoid the pitfalls of reclassification. Consulting with tax professionals and staying informed about regulatory changes can further ensure compliance and optimize tax outcomes.

Michael Holland is a Partner at Blick Rothenberg

Navigating the UK tax system can be hard enough, but having to also consider the application of the US tax rules can become too much for many transatlantic taxpayers. I work solely with business owners exposed to UK & US tax with the primary goal of ensuring their tax situations on both sides of the Atlantic are synchronised and their worldwide tax is minimised.

I work closely with Americans to help them understand, coordinate and simplify their personal and business tax affairs while guiding them through their annual tax filing obligations. I also support UK businesses to comprehend and fulfil the US tax obligations associated with expanding into the US market.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.